(Part 2)

This article discusses how to post Payroll Protection Program (PPP) Loan income and expenses in accounting software, if you are not opening a separate bank account for the funds.

In Part I of this discussion, we focused on how to post PPP funds into your accounting software if there is a separate bank account for the funds. Once again, in this article, I have teamed up with my colleague Diana Cohn of Corner Office to detail ways to book income and expenses related to the PPP from the SBA.

Note: This article does not go into detail about who is eligible or how to apply for these funds. Instead, we focus on entries to make in your accounting software of choice, once the PPP loan funds have been received and spending has started. All examples use QuickBooks (desktop and online) as the accounting software, so modify accordingly if you use a different program.

Also, keep in mind that every business has different plans for how best to use their PPP funds, so this article will address only the most basic scenario: spending at least 75 percent of PPP funds on payroll costs, and up to 25 percent of the funds on other allowable expenses. See the section at end of this article on PPP allowable expenses. Note: Our suggestions are not the only way to track PPP funds – we are just offering a scenario we have tried our best to test in QBD and QBO.

PPP Loan Income Setup – When Not Opening a Separate Account

To our understanding, whether or not you have to open a separate bank account for your PPP funds is determined by your PPP lender. If you are not opening a separate bank account, read on for what to do in QuickBooks. Many of the steps are the same as what we listed in Part I of this series, but we will repeat them here.

Setting Up the Loan Account

This loan will be a Liability (not free Income) until you determine how much of the loan will be forgiven. As such, you need to create a loan Liability account on the Chart of Accounts.

Use your judgement to determine if this is an “Other Current Liability” (usually repaid in less than a year), or a “Long Term Liability” account; we recommend the latter.

For QB Desktop(QBD): Chart of Accounts | (Ctrl+N) | Other Account Types | Other Current Liability OR Long Term Liability | Continue

Account Name: PPP Funds | Save & Close

For QB Online: Accounting | Chart of Accounts | New | Account Type: Other Current Liability OR Long Term Liability | Detail Type: Loan Payable OR Other Long Term Liabilities

Account Name: PPP Funds | Save & Close

Now you’re ready to start recording PPP spending. Note: We strongly recommend creating a spreadsheet in parallel with QuickBooks, to track PPP spending. See spreadsheet section later in this article.

Write a Check from the Business Checking for the Full Amount of the PPP Loan

This is an odd instruction, and not something a bookkeeper or accountant would normally recommend, so let’s look at the purpose of this procedure.

A. Write a check payable to the PPP Lender from the Business Checking (the account to which the PPP were direct deposited) for the full amount received. Tip: Make the check number of this check “PPP Check.”

B. Post-date the check to 8 weeks (56 days) after the date the direct deposit was received.

We will call this check the “PPP check.”

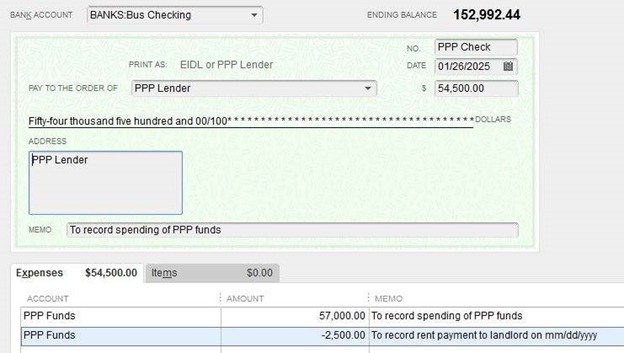

Example: The business received $57,000 in PPP funds on April 25, 2020. Write a check payable to the PPP Lender for $57,000 and date the check June 20, 2020. In QBD and QBO, the bank register will display the PPP check separated by a dark horizontal line, since the PPP check at a later date than today’s date.

Screenshot From QBD Sample Company File

Your Business Checking register will look like this:

Start Spending PPP Funds

Enter payroll and bills in the manner you would normally enter them in QuickBooks – there is no change in procedure. What is different, is that for each allowable expense, you will:

1. Add the expense to the PPP Check.

2. Add the expense to a spreadsheet (discussed further below).

Each time PPP funds are spent, edit the PPP check to add the spending on a new row, as a negative amount.

For example: $2,500 in Rent is paid. Rent is an allowable expense. Enter the rent to the landlord in the way it is normally entered in QB (Write Check, or Enter Bill/Pay Bill). Then edit the PPP check to reduce the PPP amount by the rent payment amount.

The Business checking register will now look like this:

And the PPP check will now look like this:

As expenses are deducted from the PPP check, the PPP check balance goes down, so the check balance reflects the amount of PPP funds remaining.

Tip: In QBD, as you add more spending to the PPP check, click the Recalculate button before clicking Save & Close.

Recording Spending of PPP Funds on Payroll

Allowable PPP expenses for payroll includes:

- Gross Wages

- Employer-paid State Taxes

- Employer-paid employee benefits

Note: Non-allowable payroll expenses include:

- Net Pay for Direct Deposits or manual checks

- Remittance of employee-withheld payroll taxes

- Employee wage garnishments

- Employer-paid Federal Taxes

- Payroll service fees

- Employee expense reimbursements

- Payments to Independent Contractors paid by the payroll service provider

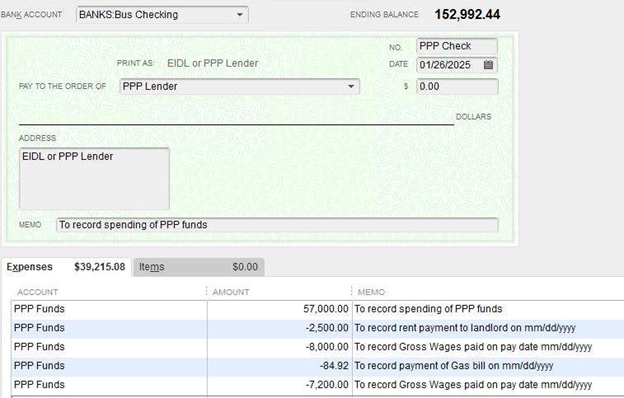

In most cases, the State Taxes paid will be negligible, so consider recording the largest payroll expense, Gross Wages, in the PPP check. For most small businesses, these funds will quickly be used up within the 8-week period.

Example: if the first payroll run since receipt of PPP funds includes $8,000 in Gross Wages, subtract that amount on the PPP Check.

Screen Shot of Ongoing Spending/PPP Check

PPP Recordkeeping

Create a folder to store electronic copies of all payroll documents and bills paid by PPP funds. Name the folder something like “PPP Spending Backup Documents.” As the 8 weeks progress, save to this folder:

- A copy of each payroll report which includes payroll costs covered by PPP funds

- A copy of each Vendor Bill paid by PPP funds

The PPP lender will request this backup documentation, so it will prove handy to have it all in one easy-to-access location.

PPP Spreadsheet

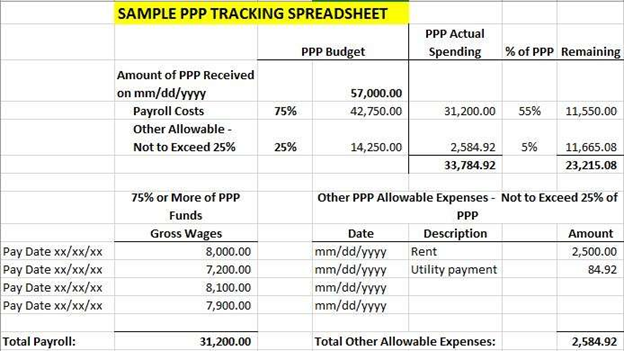

The QB P&L will not show regular spending vs. PPP spending, so keep a separate spreadsheet to track the PPP spending. Update the spreadsheet each time a new expense is added to the PPP check.

Here is a sample which shows the example of $57,000 in PPP funds received, and $33,748.92 spent-to-date. This format shows the 75 percent/25 percent breakdown, dollars spent, and dollars remaining.

PPP Loan Liability

Once all the PPP funds are depleted, the lender will audit the PPP spending using the backup documents the business saved in the “PPP Spending Backup Documents” folder. The loan will either be forgiven in full, or the lender will disallow some expenses, and require a portion of the loan to be repaid.

1. If Entire PPP Loan is Forgiven

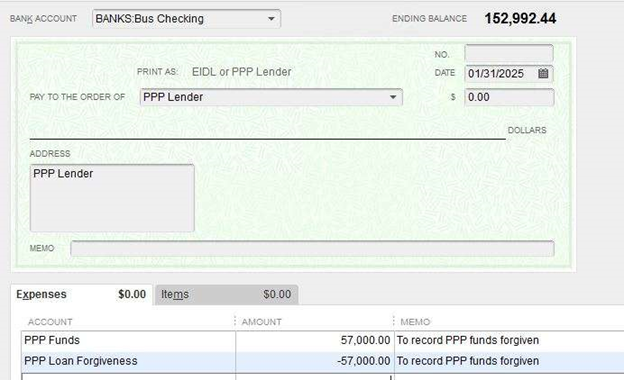

If $57,000 in PPP funds was received, and all $57,000 was spent on allowable expenses, the entire loan will be forgiven.

The PPP check in the Bus Checking register will now be a zero dollar check. To zero out the balance of the PPP Funds Liability on the Balance Sheet, create a Journal Entry or a zero dollar check to relieve the loan liability.

Create an Other Income account called: PPP Loan Forgiveness

A zero dollar check will look like this:

If creating a Journal Entry:

DR: PPP Funds

CR: PPP Loan Forgiveness

To record PPP funds forgiven

2. If Only a Portion of the Loan is Forgiven

If only a portion of the loan is forgiven by the lender, say $45,000 of the $57,000, then make the Journal Entry or zero dollar check for $45,000 and $-45,000. The Balance Sheet will show the $12,000 still due in the PPP Funds Liability account as $12,000 due.

PPP Eligible Expenses

Here are PPP guidelines copied directly from the Treasury.gov website.

What can these loans for be used for?

Your clients should use the proceeds from these loans on their:

• Payroll costs, including benefits

• Interest on mortgage obligations, incurred before February 15, 2020

• Rent, under lease agreements in force before February 15, 2020

• Utilities, for which service began before February 15, 2020.

What counts as payroll costs?

Payroll costs include:

• Salary, wages, commissions, or tips (capped at $100,000 on an annualized basis for each employee)

• Employee benefits including costs for vacation, parental, family, medical, or sick leave; allowance for separation or dismissal; payments required for the provisions of group health care benefits including insurance premiums; and payment of any retirement benefit

• State and local taxes assessed on compensation

• For a sole proprietor or independent contractor: wages, commissions, income, or net earnings from self-employment, capped at $100,000 on an annualized basis for each employee

Note From the Authors

Remember, an employer must use at least 75 percent of the PPP loan for payroll costs, or the dollar amount of forgiveness will be reduced by the amount of the shortfall. The remaining 25 perent must be used for the other covered expenses.

Conclusion

As we all know, things are changing daily, and it is difficult to stay abreast of all the news. We hope you find these suggestions and ideas useful. Please feel free to use the Comment section if you have alternate ideas, or find flaws in our presentation so we can correct them. Coming Soon: Part III: How to Use Class Tracking to Track PPP Funds.

Jody Linick is an AIPB Certified Bookkeeper, a QuickBooks® Certified Pro Advisor, and a member of the Intuit Trainer/Writer network. Her company, FitBooks Pro [www.fitbookspro.com] (formerly called Linick Consulting), specializes in remote bookkeeping services for professional services firms using QuickBooks Online. You can find her series of Blog posts here.

Diana Cohn started the Corner Office [https://www.corner-office.com/] in 1995 with the mission to teach small business owners and their staff how to use software to their advantage with the goal of achieving accuracy, efficiency, and of course, sustainable processes that create opportunities for growth. By maintaining Intuit Certifications since 1999, as well as, attending QB Connect and Scaling New Heights, Diana remains current in applications and continues to provide support for her clients and associates.